May 03•13 min read

King Dollar Isn’t Getting Dethroned Anytime Soon

De-dollarization.

The new flavor of the month for the financial pundits and talking heads.

The debt ceiling and the Fed’s Bank Term Funding Program (BTFP) are so yesterday. The United Kingdom just posted a red-hot inflation reading of 10.1% that barely moved any needles.

And yet, the attention of the majority of social media platforms still fixate on the efforts of countries around the world trying to move away from the dollar.

How valid are the recent de-dollarization attempts that we have seen in the past few weeks? What does it mean to the global economy should the dollar lose its reserve currency status? How will other assets perform if this happens?

Today, let’s observe how this battle for king of the hill will shape up.

Ben Lilly here.

For those who have been looking for a new exchange, consider checking out ByBit.

They operate in 160 countries. They have more than 270 assets trading on spot and over 200 perpetual and quarterly futures contracts. They even offer options contracts and NFT trading.

Simply put, ByBit has a lot to offer any trader. And right now, they are offering a $10 welcome bonus if you open a new account and complete some introductory tasks. They also have additional ways for you to earn.

If you are looking for a new platform to trade on, consider ByBit today by clicking here. Also, if you simply want to support Espresso and the Jarvis Labs team, consider giving a click.

How King Dollar Earned Its Crown

If you’re an iPhone user, you probably know that they’re not produced in the U.S. Most of them are built in China.

But even that’s not completely accurate. Making an iPhone involves a supply chain that includes over 43 countries.

Imagine the amount of time, effort, and paperwork involved if all 43 countries used their own currency for pricing and payment.

How efficient would that be?

A single currency that acts as a global reserve that countries can use for trade solves this problem. Without USD as the top dog, most likely we would not have seen global trade expand the way it did.

So how did the dollar rise to the top?

In the 1970s, the combination of USD depegging from the gold standard and the petrodollar arrangement with Saudi Arabia propelled the dollar to become the de facto global reserve currency.

Without the gold peg, the U.S. Treasury could continue to print money no matter how much gold is in its vault. That provided more liquidity to the market.

With the new liquidity, the arrangement with Saudi Arabia forced every country in the world to use USD to buy oil from Saudi Arabia and OPEC. That led to all global commodities, not just oil, gradually becoming priced in USD, which continues to this day.

And since the U.S. is the largest consumption market in the world, everything that gets shipped into the U.S. is priced in USD. (It also doesn’t hurt that the U.S. has the world’s largest and strongest military.)

It is not a stretch to say the globalization of the world’s economy was only possible because of the dollar’s status as the global reserve currency. USD provided the entire world with a common, trusted medium of exchange that enabled countries to trade using a uniform standard.

But why could we not have another currency as a companion or replacement to the dollar as the global reserve currency?

For starters, check out the chart below.

Source: BDSwiss

USD is the most popular currency for foreign reserves held globally, making it the most liquid commodity in the world.

As a result, the dollar can be freely traded, held, bought, and sold anytime and anywhere. Anyone can exchange USD anywhere in the world for local currency or use it to barter for goods. Its huge volume of liquidity and universal acceptance are the most desired attributes for a reserve currency.

But also, the issuing entity of a reserve currency needs to provide yield-earning instruments with high liquidity to incentivize other countries to hold on to the reserve currency.

That’s why anyone can exchange the dollar for U.S. Treasurys to earn yields. U.S. Treasurys are considered to be some of the safest, most liquid interest-bearing investment vehicles in the world.

This incentivizes countries to hold USD in their foreign reserves so they can buy Treasurys to earn interest. And should they need to liquidate for fundraising purposes, there will always be demand for them.

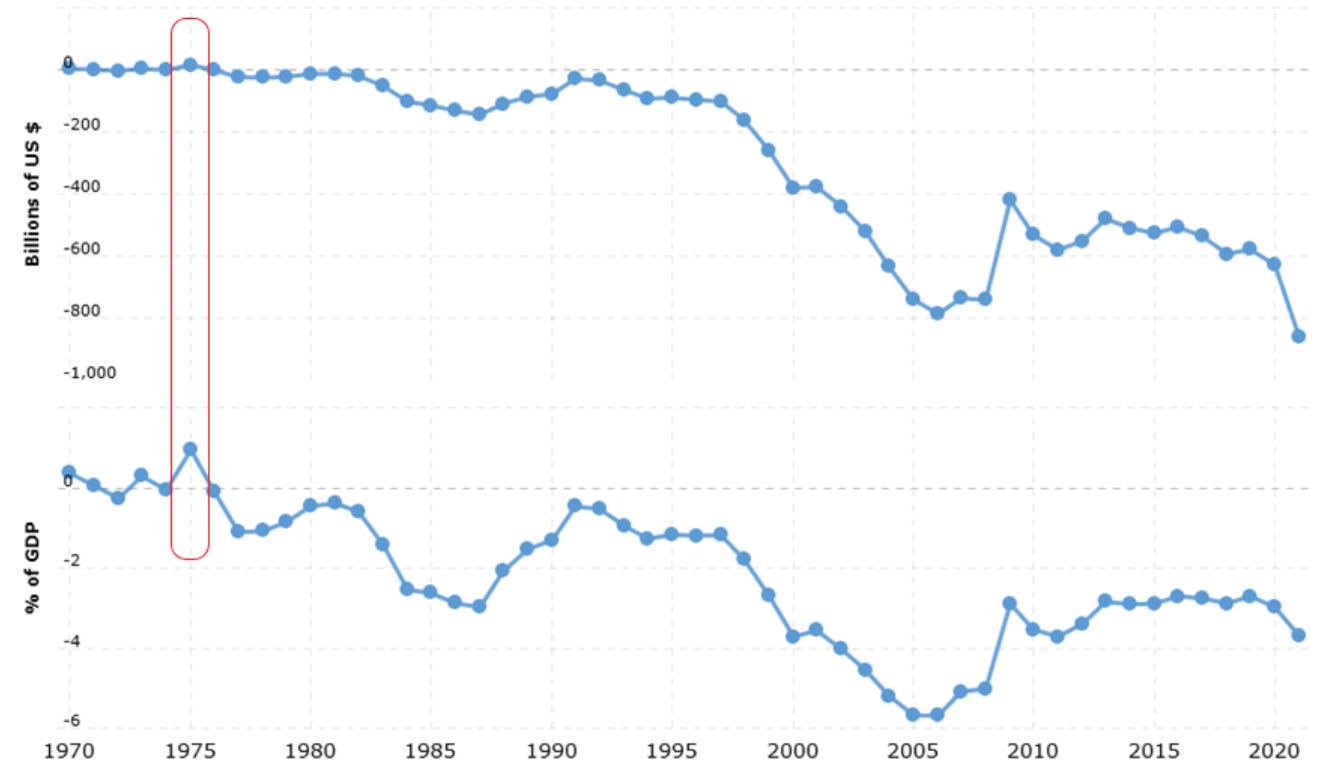

Last but not least, the issuer of a global reserve currency has to run a trade deficit. It must have an economy that is big and robust enough to absorb all the excess production surplus from the rest of the world and run a negative balance on international trade.

Below is a chart of the U.S. trade balance from 1970 to 2021, measured both by amount and as a percentage of GDP. The red outline highlights the last time the U.S. had a trade surplus, which was in 1975.

Source: www.macrotrends.net

In fact, in 2022, the U.S. had the highest trade deficit ever at $948.1 billion.

The U.S. is the only economy that is robust enough to handle this burden of taking all the excess surplus from other countries in order to boost the global economy.

But lately, efforts to decrease USD dependence and dethrone the dollar as the global reserve currency have been picking up steam.

Jostle for the Top

As the global reserve currency issuer, the U.S. has a tremendous amount of influence globally.

The rumbles to unseat USD, weaken its dominance, or reduce dependence on it is nothing new.

But with the sanctions imposed on Russia by the U.S. because of the Ukraine invasion, the U.S. essentially weaponized the dollar.

This is a bit of a wake-up call for other countries in the world.

What the U.S. sanctions did is demonstrate to the world the consequences of holding USD should any country’s ideas or politics be diametrically opposed to that of the U.S. And it’s incentivized countries to start moving trades away from the dollar.

Naturally, the next question will be: What currency could eventually take the place of USD as the global reserve currency?

Here are the three most talked-about contenders.

The Rise of the Chinese Yuan?

The winner of the popularity contest lately seems to be the Chinese yuan (CNY), also known as the renminbi (RMB).

Putin recently stated that all commodity exports from Russia will be settled in CNY instead of the ruble (it might be an indication of the progress of the Ukraine War – but we will let the geopolitical experts decipher this one). Saudi Arabia has begun to accept payments in CNY for crude. Brazil also joined the CNY party by allowing commodity exports to be settled in CNY.

Meanwhile, the U.S. had an “Et tu, Brute!?!” moment when France announced that it will be buying liquefied natural gas from China and agreed to settle the trades in CNY.

Will CNY ascend and displace USD as the global reserve currency?

It’s possible, but not probable.

First, China’s capital market is still closed to the rest of the world. CNY is not freely traded because the Chinese Communist Party is seriously concerned about capital flight (for good reasons) should they open the Chinese capital market and let CNY freely float and trade against other currencies. Don’t expect this to change for CNY anytime soon.

Next, will the rest of the world be willing to hold Chinese government debts? After all, if all the trades going into China are denominated and settled in CNY, the trading partners will end up with a tremendous amount of CNY.

Buying Chinese Treasuries is an option. The Chinese bond market is the third-largest in the world, growing to over $13 trillion in 2020.

But the interesting thing here is that even though Fitch and other rating agencies give Chinese Treasuries top marks, the Chinese government still holds the majority of them.

Foreign investors’ presence in China’s onshore bond market remains small, accounting for only 3.2% of the total holdings.

This means Chinese Treasuries aren’t very liquid. And to top it off, it is not a free economy. The state controls everything, including the bond market. This does not sit well with investors.

The appeal of a yield-earning instrument for CNY holders is just not there for now.

How about using CNY to buy widgets and trinkets from China? Most of the countries exporting to China are probably looking to use that newly acquired CNY for items in the high-tech, defense, and heavy industries.

Will Saudi Arabia want to buy anti-air missiles from China instead of the U.S.? Will France want to buy semiconductor chips from China?

Maybe. Maybe not. This is another potentially worrying issue for the countries that are going to start settling trades in CNY.

Lastly, China will not and cannot run a trade deficit.

Below is a table of countries with the highest trade surpluses in 2021.

Source: worldstopexports.com

China will have to continue running a trade surplus to keep its economy running. It needs to produce goods and keep exporting to the rest of the world.

Overall, the CNY still has a long way to go before it can be considered as a replacement for the dollar.

Can Gold Make a Comeback?

Gold has seen a bit of a renaissance in the past few months.

Multiple countries have disclosed that they’ve added gold to their existing holdings:

China added 32 tonnes in 2022, with a total of 1,980 tonnes as of November.

Russia has increased its gold holdings by 1 million troy ounces since invading Ukraine.

Singapore added 44.6 tonnes in January this year, boosting its holdings to a total of 198.4 tonnes.

Other countries are probably quietly acquiring it under the radar.

This had gold bugs jumping for joy and the talk of going back to a gold standard gaining momentum.

But the gold standard has several problems of its own.

Any type of asset-backed monetary policy, fractional or not, is subject to the amount of assets held. Simply put, in the gold standard, if a nation has 100 tons of gold, it cannot issue more than a proportional amount of currency, unless the nation purchases more gold to add to its reserve.

This makes credit expansion a thing of the past. And no nation in the world will be willing to go back to the asset-backed currency system and forgo the ability to increase and expand credit facilities infinitely.

With curbed credit expansion, global trade will slow down drastically. The trading and economic growth that took place in the past three decades will grind to a halt. Moving forward, it might not be the best monetary policy to jumpstart the global economy.

Cryptocurrencies – The New Kids on the Block

Could Bitcoin (BTC) or Ethereum (ETH) be the answer?

The features offered by traditional cryptocurrencies fit the bill quite well: Trustless, permissionless, and decentralized, although whether they’re truly decentralized remains to be determined.

But if BTC or ETH ever gains mass adoption, this means governments will lose control of finance and banking control over their citizens.

And they will not allow this to happen.

What traditional cryptocurrencies can offer is an alternative monetary system that enables an alternative, underground economy to operate and thrive alongside the official one.

We don’t need to look far into the future to imagine this, because it is playing out right now before our eyes.

Citizens in countries such as Lebanon and Nigeria are currently using cryptocurrencies as an alternative monetary system, because the fiat systems from their governments have all but frozen up.

The Devil We Know

In the near term, it is all about the devil we know.

The dollar is still a stabilizing agent that keeps the global economy together – for now.

Will USD ever lose the global reserve currency status? Sure. Nothing lasts forever.

But timing is the question here. How fast or slow will it take? It depends on how the current geopolitical factors play out.

But for those waiting to see the day that USD gets dethroned, it is probably best not to do it with bated breath.

What USD is to the global financial system is just like what palm oil is to our daily goods.

It is ubiquitous and ever-present.

If you’re a gold bug, don’t get too excited. Remember, gold futures contracts are still denominated in USD.

As for the BTC maxis, if you want to spend your profits at the local Lamborghini dealer, you still have to off-ramp into USD.

That is why we have USDT, USDC, or BUSD, but we don’t see stables issued in the Japanese yen, Indian rupee, or Chinese yuan.

As an anecdote, depending on which expert provides the opinion, the notional balance of the entire global derivatives market ranges from $600 trillion to $1 quadrillion USD.

That is a lot of money and derivative contracts.

And they are all denominated in U.S. dollars.

It will be impossible to unwind all those contracts in CNY or BTC.

While all the gold enthusiasts, crypto zealots, and other anti-USD pundits are champing at the bit, the point is: USD is not going to lose global reserve currency status anytime soon. It will happen, but not in the immediate future.

It will be a slow and most likely chaotic process.

Should USD be displaced with no heir apparent in sight, expect a tempest of confusion and chaos in the global financial market.

For instance, India just overtook China as the most populous nation in the world. She has the largest consumer base in the world now. And with its continued border disputes and military skirmishes with China in the region of Kashmir, why would India be willing to accept CNY as the new global reserve currency?

As a global superpower, India will want to put up a fight for global reserve currency status.

Brazilian President Lula also recently voiced his opinion:

Every night I ask myself why all countries have to base their trade on the dollar. Why can’t we do trade based on our own currencies?

This is akin to kids fighting over their inheritance in front of the dying parent.

The BRIC nations can’t even agree on a universal global reserve currency.

Sometimes, it is better to stick with the old devil we know.

Yours truly,

TD

This newsletter is sponsored by Bybit. Be sure to try out the exchange here, and take advantage of all they have to offer today.